Blog Retirement Planning

What Are Retirement Gap Years? Timing Social Security, Roth Moves, and Medicare When people hear “gap year,” they often think of the year between high school and college. But there’s another kind of gap year that can have a big financial impact: the years between retiring and starting Social Security or pension income. These retirement…

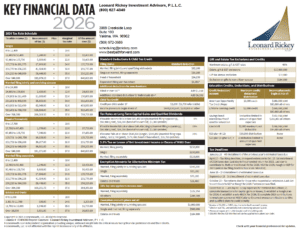

The annual exclusion for gifts remained at $19,000 for 2026. The limitation on deferrals for 401(k), 403(b), and 457 plans is increased to $24,500 for 2026, up from $23,500 in 2025. The catch-up for those over age 50 was increased to $8,000 from $7,500, so if you are maxing out your plan and over age…

Starting January 1, 2026, a change under the SECURE 2.0 Act will affect how some employees age 50 and older make catch-up contributions to their workplace retirement plans. What’s Changing? If you turn 50 or older in 2026 and your 2025 FICA wages (Box 3 of your W-2) with your current employer were over $150,000*,…

Starting in January 2026, Social Security beneficiaries will receive a 2.8% cost-of-living adjustment (COLA) designed to help benefits keep pace with inflation. The adjustment is based on the Consumer Price Index, reflecting changes in the cost of goods and services over the past year. Beneficiaries will be notified of their new benefit amounts by mail…

You still have time to contribute to your Traditional IRA, Roth IRA, SEP IRA, and HSA accounts for 2024. Contributions are due by the earlier of April 15, 2025, or the filing date of your tax return. For 2024, you can contribute up to $7,000 to your Traditional or Roth IRA and an additional $1,000…

Starting in January 2025, Social Security beneficiaries will receive a 2.5% cost-of-living adjustment (COLA) designed to help benefits keep pace with inflation. The adjustment is based on the Consumer Price Index, reflecting changes in the cost of goods and services over the past year. In addition, the maximum amount of earnings subject to Social Security…

Social Security recipients are getting a 3.2% increase in their 2024 benefits. The Medicare Part B premium is increasing from $164.90 to $174.70 per month. The annual exclusion for gifts increases to $18,000 from $17,000 per year per individual. The limitation on deferrals for 401(k), 403(b), and most 457 plans is increased to $23,000 for…

Starting January 2024, Social Security beneficiaries will receive a 3.2% cost-of-living adjustment (COLA). The adjustment is calculated based on inflation as measured by the Consumer Price Index. The maximum amount of earnings subject to the Social Security tax (taxable maximum) will increase to $168,600 from $160,200. Social Security beneficiaries are normally notified by mail or through…

SECURE Act 2.0 was signed into law at the end of 2022 as a follow up bill to the original SECURE Act that was signed into law in 2019. SECURE 2.0 targets several retirement provisions that go into effect over the next 10 years. We will focus on the changes for this year and continue…

Medicare beneficiaries can make new choices and pick plans that work best for them during the annual Medicare Open Enrollment Period. Each year, Medicare plan costs and coverage typically change. In addition, your health-care needs may have changed over the past year. The Open Enrollment Period — which begins on October 15th and runs through…