Sep 15, 2022 The Huge Cost of Doing Nothing

One of the biggest decisions when transitioning into adult life is when to start saving. Putting off savings till later comes with a cost of waiting. Cost of waiting describes the opportunity cost when an individual decides to wait before beginning to save money. This cost can result in a smaller portfolio at retirement, larger contributions later in life to catch-up, or a lower standard of living.

Savings should be compared to running a marathon. The sooner you get started, the better off you will be reaching the finish line. By starting to save early in life, you gain an overwhelming advantage over those who wait later due to the time value of money. Time value of money is an essential component of finance. “A dollar today is worth more than a dollar tomorrow.” A dollar received today is worth more because that dollar can be invested, earn interest, and eventually compound in value. It has an opportunity value that a dollar tomorrow doesn’t have.

A quote commonly attributed to Albert Einstein says that “Compounding interest is the eighth wonder of the world.”

Compound interest can be extremely powerful for investors over time. Compounding interest essentially results in interest on interest, and it’s why so many long-term investors have been successful.

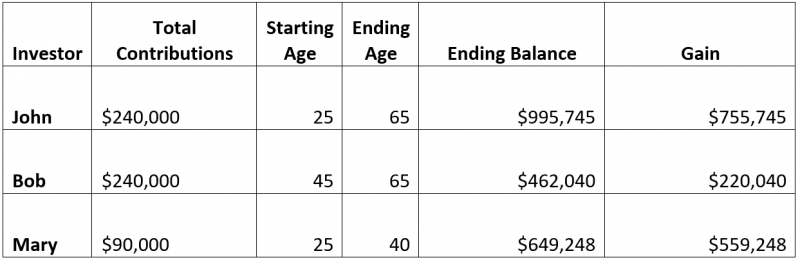

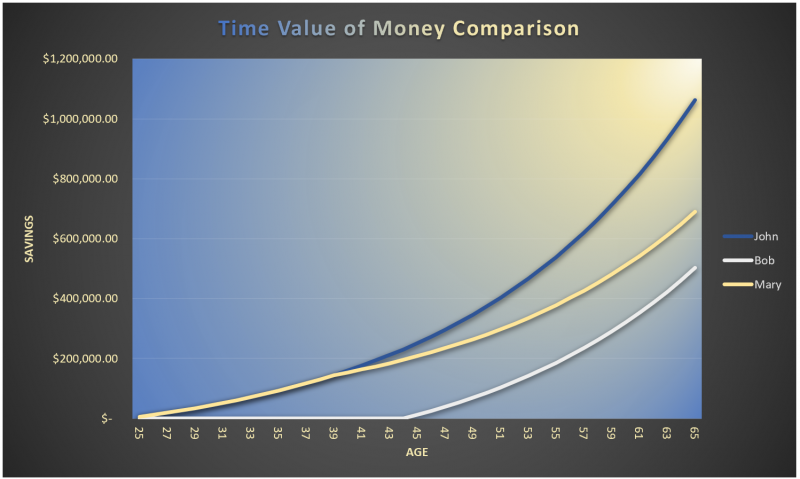

To demonstrate this, consider the fate of three investors. John, Bob and Mary. Each have a hypothetical 6% return (compounded monthly) and 40 years to save for their goal. For the sake of simplicity, the effect of taxes is ignored on this example.

At the age of 25 John starts saving for retirement with the plan to retire at 65. If John contributes $6,000 per year ($500 per month) into an account every year for 40 years by time John is 65 he has accumulated almost one million dollars ($995,745).

Now let’s look at it from an individual who decides to wait. Bob decided to wait on putting money aside until age 45. He was busy getting his career and family started. However, but has more disposable income so he can start putting away $1,000 per month. Over the next 20 years Bob will save the same amount of money as John ($240,000) but only accumulate $462,040 towards his goal.

Lastly, let’s look at an individual who starts saving early and then stops. Mary starts saving to her savings account at age 25 with the goal of retiring at age 65. However, Mary’s financial priorities change, and she stops saving at age 40. She has only saved $90,000 towards her goal but will still have 45% more saved than Bob. Her account balance of approximately $649,248 takes advantage of compound interest over the entire 40-year period.

The moral of the story is that it pays to start saving as early as you can. It is worth much more than waiting to save more when your income is higher.

Company News

Market Commentary

Retirement Planning

Tax Planning

Cyber Security

Important Disclosures

Leonard Rickey Investment Advisors, PLLC (“LRIA”), is an SEC registered investment adviser located in the State of Washington. Registration does not imply a certain level of skill or training. For information pertaining to the registration status of LRIA, please contact LRIA or refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov).

This is provided for general information only and contains information that is not suitable for everyone. As such, nothing herein should be construed as the provision of specific investment advice or recommendations for any individual. To determine which investments may be appropriate for you, consult your financial advisor prior to investing. There is no guarantee that the views and opinions expressed herein will come to pass. This newsletter contains information derived from third party sources. Although we believe these third-party sources to be reliable, we make no representations as to the accuracy or completeness of any information prepared by any unaffiliated third party incorporated herein and take no responsibility therefore.

Any projections, forecasts and estimates, including without limitation any statement using “expect” or “believe” or any variation of either term or a similar term, contained here are forward-looking statements and are based upon certain current assumptions, beliefs and expectations that LRIA considers reasonable or that the applicable third parties have identified as such. Forward-looking statements are necessarily speculative in nature, and it can be expected that some or all of the assumptions or beliefs underlying the forward-looking statements will not materialize or will vary significantly from actual results or outcomes. Some important factors that could cause actual results or outcomes to differ materially from those in any forward-looking statements include, among others, changes in interest rates and general economic conditions in the U.S. and globally, changes in the liquidity available in the market, change and volatility in the value of the U.S. dollar, market volatility and distressed credit markets, and other market, financial or legal uncertainties. Consequently, the inclusion of forward-looking statements herein should not be regarded as a representation by LRIA or any other person or entity of the outcomes or results that will be achieved by following any recommendations contained herein. While the forward-looking statements here reflect estimates, expectations and beliefs, they are not guarantees of future performance or outcomes. LRIA has no obligation to update or otherwise revise any forward-looking statements, including any revisions to reflect changes in economic conditions or other circumstances arising after the date hereof or to reflect the occurrence of events (whether anticipated or unanticipated), even if the underlying assumptions do not come to fruition. Opinions expressed herein are subject to change without notice and do not necessarily take into account the particular investment objectives, financial situations, or particular needs of all investors.

For additional information about LRIA, including fees and services, please contact us for our Form ADV disclosure brochure using our contact information herein. Please read the disclosure brochure carefully before you invest or send money.

2026 1st Quarter Investment Commentary