Apr 13, 2021 Economic Analysis & A Note on Inflation

Economic Analysis

As was the case in 2020, the pandemic’s course should dictate the course of the economic expansion in 2021. As vaccines continue to be administered, it seems likely that the economy will re-open and continue its recovery. This, along with massive stimulus, could propel the economy to growth not seen in decades. An additional $1.9 trillion in pandemic relief was signed into law in March, including additional direct payments to households to help provide a bridge to the end of the pandemic. This brought the total U.S. stimulus to roughly $5 trillion in just the last year (9). There is potential for an additional $3 trillion infrastructure bill later this year.

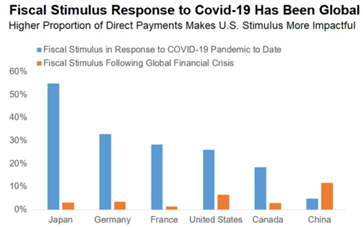

The chart illustrates just how massive this stimulus is relative to the size of major economies and also how much larger it is compared to the Global Financial Crisis (10). For example, U.S. stimulus in response to COVID-19 is equivalent to about 26% of US GDP.

On aggregate, the stimulus more than compensated consumers for their income shortfalls related to the pandemic shutdown. Consequently, household disposable income grew faster last year than during most growth booms and left household balance sheets in very good condition. Although support for corporations was a little less overwhelming, it still allowed firms to weather the recession in relatively good shape.

As a result, the economic backdrop appears more robust than it was following the 2008 recession. A variety of metrics measuring employment, manufacturing, and inflation expectations were increasing faster than in prior recoveries. And, unlike the last recession, household and corporate balance sheets are in good shape. Home prices have been strong, increasing at their fastest pace in 15 years (11), and consumer savings rate reached record highs.

There are significant risks with all of the stimulus, including higher government debt, higher taxes, higher interest rates, and higher inflation. Also, U.S. consumer psychology may be different post-pandemic, and consumers may not return to pre-pandemic spending rates as soon as they are able.

A Note on Inflation

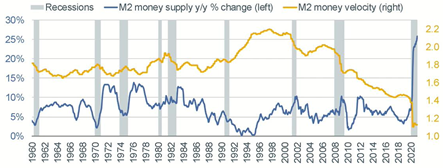

Inflation has moved to the front of the queue of potential risks. The unprecedented fiscal and monetary expansion being deployed has lead to rapid growth of the money supply and credit. Policymakers have repeatedly said they are not worried about inflation and view low inflation as the more immediate threat. Currently, the data agree – the latest Consumer Price Index came in at only 1.7%, mainly due to the low velocity of money (see chart (12)). The velocity of money is the rate of turnover in the money supply or how quickly consumers and businesses spend money (versus saving it or investing it). Over the longer term, the risk of inflation appears skewed to the upside.

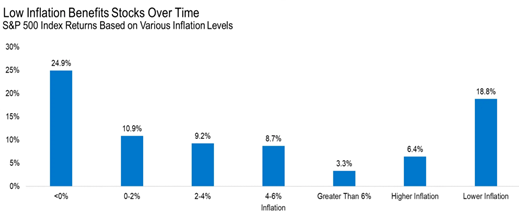

Historical data suggest that stocks have positive returns during higher inflation environments, but they do best in low inflation environments like we have had over the past ten years (see chart). Taking it a step further, if inflation is trending lower, then stocks do better (18.8% on average) versus if inflation is trending higher (6.4% on average) (13). Further research from both Blackrock and J.P. Morgan shows that value equities and emerging market equities have historically outperformed in higher inflationary regimes.

Please reach out to your advisor if you have any questions or concerns.

[9]Business Insider, March 10, 2021

[10]LPL Research

[11]Wall Street Journal, S&P CoreLogic Case-Shiller Index

[12]Charles Schwab, as of 1/31/2021

[13] LPL Research, 1950-2020. Higher or lower inflation is based on if inflation has increased (or decreased) from the prior year’s levels for more than 3 consecutive years

INDEX DEFINITIONS

The Barclays Aggregate Bond Index represents securities that are SEC-registered, taxable, and dollar denominated. The index covers the US investment-grade fixed rate bond market, with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securities.

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. It cannot be invested into directly.

The Russell 2000 Index is an unmanaged index generally representative of the 2,000 smallest companies in the Russell Index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index.

The MSCI Emerging Markets Index is a float-adjusted market capitalization index that consists of indices of approximately 800 stocks and is designed to measure equity market performance in 23 emerging economies: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Korea, Malaysia, Mexico, , Peru, Philippines, Poland, Qatar, Russia, South Africa, Taiwan, Thailand, Turkey, and the United Arab Emirates.

The MSCI EAFE (Europe, Australasia, Far East) Index is a free float-adjusted market capitalization index of approximately 900 stocks and is designed to measure equity market performance in 21 developed market countries outside of North America.

The SG Trend Index is a subset of the SG CTA Index, and follows traders of trend following methodologies. The SG CTA Index is equal weighted, calculates the daily rate of return for a pool of CTAs selected from the larger managers that are open to new investment.

Swiss Re Global Cat Bond Index tracks the aggregate performance of all catastrophe bonds issued offered under Rule 144A. The index captures bonds denominated in any currency, all rated and unrated cat bonds, outstanding perils, and triggers. The index is not exposed to currency risk from non-USD denominated cat bonds.

The Dow Jones Industrial Average® (The Dow®), is a price-weighted measure of 30 U.S. blue-chip companies. The index covers all industries except transportation and utilities.

The Dow Jones Transportation Average is a 20-stock, price-weighted index that represents the stock performance of large, well-known U.S. companies within the transportation industry.

Company News

Market Commentary

Retirement Planning

Tax Planning

Cyber Security

Important Disclosures

Leonard Rickey Investment Advisors, PLLC (“LRIA”), is an SEC registered investment adviser located in the State of Washington. Registration does not imply a certain level of skill or training. For information pertaining to the registration status of LRIA, please contact LRIA or refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov).

This is provided for general information only and contains information that is not suitable for everyone. As such, nothing herein should be construed as the provision of specific investment advice or recommendations for any individual. To determine which investments may be appropriate for you, consult your financial advisor prior to investing. There is no guarantee that the views and opinions expressed herein will come to pass. This newsletter contains information derived from third party sources. Although we believe these third-party sources to be reliable, we make no representations as to the accuracy or completeness of any information prepared by any unaffiliated third party incorporated herein and take no responsibility therefore.

Any projections, forecasts and estimates, including without limitation any statement using “expect” or “believe” or any variation of either term or a similar term, contained here are forward-looking statements and are based upon certain current assumptions, beliefs and expectations that LRIA considers reasonable or that the applicable third parties have identified as such. Forward-looking statements are necessarily speculative in nature, and it can be expected that some or all of the assumptions or beliefs underlying the forward-looking statements will not materialize or will vary significantly from actual results or outcomes. Some important factors that could cause actual results or outcomes to differ materially from those in any forward-looking statements include, among others, changes in interest rates and general economic conditions in the U.S. and globally, changes in the liquidity available in the market, change and volatility in the value of the U.S. dollar, market volatility and distressed credit markets, and other market, financial or legal uncertainties. Consequently, the inclusion of forward-looking statements herein should not be regarded as a representation by LRIA or any other person or entity of the outcomes or results that will be achieved by following any recommendations contained herein. While the forward-looking statements here reflect estimates, expectations and beliefs, they are not guarantees of future performance or outcomes. LRIA has no obligation to update or otherwise revise any forward-looking statements, including any revisions to reflect changes in economic conditions or other circumstances arising after the date hereof or to reflect the occurrence of events (whether anticipated or unanticipated), even if the underlying assumptions do not come to fruition. Opinions expressed herein are subject to change without notice and do not necessarily take into account the particular investment objectives, financial situations, or particular needs of all investors.

For additional information about LRIA, including fees and services, please contact us for our Form ADV disclosure brochure using our contact information herein. Please read the disclosure brochure carefully before you invest or send money.

2026 1st Quarter Investment Commentary